Azerbaijan becomes a single point of failure for Europe-Asia flights - March 2026

The air corridor connecting Europe to East Asia is experiencing an unprecedented level of fragility in early March 2026, as multiple overlapping airspace closures have reduced the available routing options to a dangerously narrow set of alternatives. The disruption stems from three simultaneous geopolitical crises: the ongoing Russia-Ukraine war (since February 2022), the escalation of the Iran conflict following coordinated US-Israeli strikes on February 28, 2026, and the resulting cascade of airspace shutdowns across the Gulf region.

Under normal conditions, long-haul flights between Europe and Asia follow optimized great-circle routes that cross the Middle East, taking advantage of major hub airports in Dubai, Doha and Abu Dhabi operated by carriers such as Emirates, Qatar Airways and Etihad Airways. These Gulf megahubs serve as the primary connection points between Western Europe and South Asia, Southeast Asia and Australasia. When this central corridor is functioning, a typical London-to-Singapore flight takes approximately 13 hours.

Since the Russian invasion of Ukraine in February 2022, all European Union airlines, US carriers, British airlines and most other Western operators have been banned from Russian airspace due to reciprocal sanctions. This eliminated the northern Siberian corridor, historically one of the most efficient routes between Europe and Northeast Asia. European carriers now face flight times that are one to three hours longer on routes to destinations such as Tokyo, Beijing and Singapore compared to their Chinese or Middle Eastern competitors who retain access to Russian airspace.

The situation deteriorated sharply on February 28, 2026, when US and Israeli military strikes on targets inside Iran triggered immediate retaliatory actions across the region. Within hours, airspace closures were declared over Iran, Iraq, Israel, Qatar, Bahrain, Kuwait and Syria. The United Arab Emirates largely halted civilian flights, and major hubs in Dubai, Abu Dhabi and Doha saw thousands of flights cancelled. The European Union Aviation Safety Agency (EASA) issued Conflict Zone Information Bulletin CZIB 2026-03, advising operators not to fly at any altitude over Iran, Iraq, Israel, Jordan, Lebanon, Bahrain, Kuwait, Qatar, the UAE, Oman and Saudi Arabia.

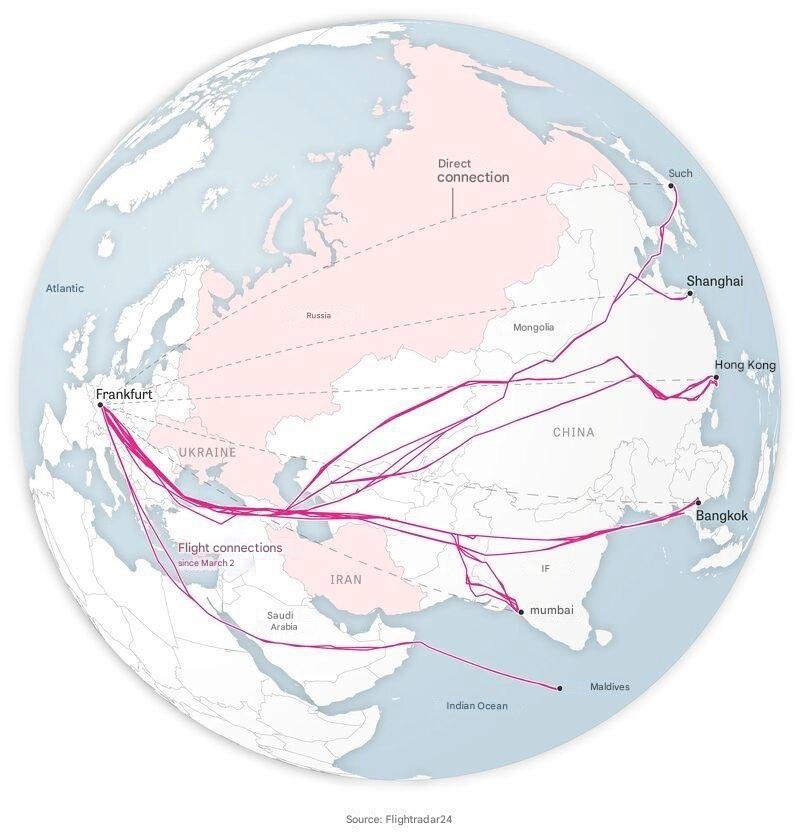

With both the northern route over Russia and the central route through the Gulf effectively blocked for Western airlines, only two bypass corridors remain. The northern alternative routes traffic through Turkey, Armenia and Azerbaijan before continuing over Central Asia and Afghanistan. The southern alternative sends flights down through Egypt, across Saudi Arabia and Oman, then onward via the Arabian Sea. Both options add between 300 and 800 nautical miles to standard Europe-Asia services, extending flight times by 45 to 120 minutes and significantly increasing fuel consumption.

Azerbaijan has emerged as a critical single point of failure (SPOF) in this rerouted network. The Armenia-Azerbaijan corridor is now one of the main bypass routes linking Europe with Asia, and traffic through the Baku Flight Information Region (UBBA FIR) has surged. However, the fragility of this chokepoint was exposed on March 5, 2026, when Iranian drones crossed into Azerbaijan's Nakhchivan exclave and struck near Nakhchivan International Airport, damaging civilian infrastructure and injuring several people. Azerbaijan temporarily closed the southern sector of the Baku FIR for 12 hours in response. Although the main overflight routes through the FIR remained available, the incident demonstrated how a single drone strike could threaten the last viable northern corridor between Europe and East Asia.

If Azerbaijan were to fully close its airspace, the consequences would be severe. Flight times from Europe to Asia could effectively double overnight. A London-to-Singapore journey would stretch from 13 hours to over 20 hours. The southern bypass via Egypt, Saudi Arabia and Oman would become the only remaining option for Western carriers, but this route faces its own constraints: parts of Saudi airspace have route-level closures due to military activity, and Oman has reported widespread GNSS interference affecting navigation systems.

The impact on air cargo has been immediate and severe. According to capacity tracking firm Rotate, Middle East airspace restrictions directly affected approximately 13 percent of global air cargo capacity. Within 24 hours of the first major flight suspensions, global air cargo capacity dropped by 18 percent compared to the previous week. On the Asia-Middle East-Europe corridor specifically, cargo capacity fell by more than 40 percent week-on-week on some routes. Industry estimates suggest that Gulf carriers collectively lost over 1 billion USD in revenue within the first five days of the crisis, with daily losses exceeding 200 million USD across the seven largest Gulf airlines.

Not all airlines are equally affected. A significant competitive asymmetry exists based on access to Russian airspace. Airlines from China (Air China, China Eastern, China Southern, Hainan Airlines, Xiamen Air), the Middle East (Emirates, Etihad, Qatar Airways), India (Air India), Turkey (Turkish Airlines, Pegasus Airlines), Serbia (Air Serbia), Belarus (Belavia), and several other Asian and African carriers retain permission to overfly Russia. This gives them a major advantage on Europe-Asia routes, with Chinese carriers in particular able to offer flights that are up to two hours shorter than their European competitors on routes such as London-Beijing.

The airlines currently authorized to use Russian airspace for Europe-Asia routing include: Air China, China Eastern Airlines, China Southern Airlines, Hainan Airlines, Xiamen Air, Beijing Capital Airlines (China), Emirates, Etihad Airways, Qatar Airways (Gulf - though currently grounded by the Iran conflict), Air India (India), Turkish Airlines, Pegasus Airlines (Turkey), Air Serbia (Serbia), Belavia (Belarus), Sri Lankan Airlines, Air Arabia, Flydubai, Uzbekistan Airways, Cham Wings (other Asian carriers), and Royal Air Maroc, EgyptAir, Air Algerie, Ethiopian Airlines (African carriers).

Regarding the southern bypass route in the event of a full Azerbaijan closure, modern widebody aircraft such as the Boeing 777 or Airbus A350 typically have sufficient range to complete most Europe-to-East Asia flights via the Egypt-Saudi-Oman-Arabian Sea routing without a technical fuel stop. However, the longer route burns an estimated 6,000 kg of extra fuel per flight, adding over 5,000 USD in fuel costs alone. For some of the longest city pairs, such as London to Sydney or Paris to Auckland, payload restrictions may be necessary to carry the additional fuel, reducing available seats or cargo capacity.

A further escalation scenario involving a direct conflict with China would represent a catastrophic disruption to Europe-Asia air connectivity. Chinese carriers currently operate a significant share of direct Europe-Asia capacity and are among the few airlines that can efficiently route via Russian airspace. If Chinese airspace were closed to foreign operators, or if Western nations imposed aviation sanctions on China similar to those applied to Russia, the resulting capacity loss would far exceed the current crisis. Routes to non-Chinese Asian destinations such as Tokyo, Seoul, Singapore, Bangkok and Hanoi would need to avoid both Chinese and Middle Eastern airspace simultaneously, leaving almost no viable direct routing options and potentially making some city pairs unserviceable without intermediate fuel stops.

As of March 8, 2026, the situation remains highly volatile. EASA's conflict zone bulletin has been extended through at least March 11, and airlines are preparing multiple backup flight plans, ready to scale operations up or down depending on how the conflict evolves. The combination of closed Gulf hubs, restricted northern corridors through the Caucasus, and elevated fuel prices following tensions around the Strait of Hormuz has created what industry analysts describe as a perfect storm for Europe-Asia aviation.

💡 Alternative Solution

Use of airlines with Russian airspace access (Chinese and Turkish carriers) for Europe-Asia connectivity