JPMorgan Maps Global Oil Shockwave from Hormuz Closure - Global Supply Crisis Timeline

JPMorgan commodity strategist Natasha Kaneva published a landmark report on March 26, 2026, outlining a detailed roadmap of how the Strait of Hormuz closure is triggering a progressive, region-by-region oil supply shock across the planet. The analysis reveals that the global oil system has shifted from a sudden flow disruption into a slow-burning inventory depletion crisis, with timing now becoming the central variable driving economic damage.

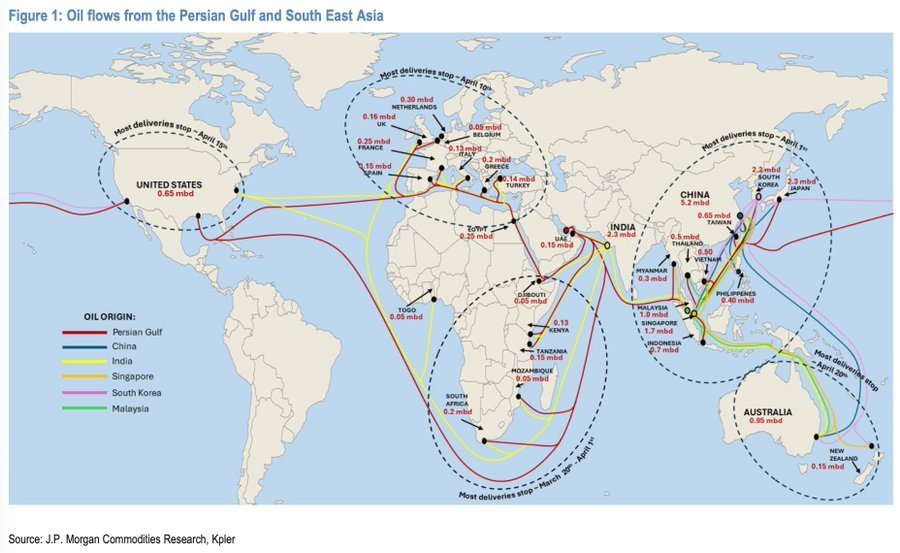

The report establishes that the last commercial tanker exited the Strait of Hormuz on February 28, the same day US and Israeli forces launched military operations against Iran. Since that date, vessel traffic through the waterway has dropped by more than 95 percent, with only a trickle of Iranian-controlled shipments passing through under tightly restricted conditions. JPMorgan estimates the initial gross supply shock at approximately 16 million barrels per day, gradually easing toward 10 million barrels per day by April as bypass routes and emergency reserves absorb part of the blow.

The shockwave is spreading from east to west, dictated by maritime shipping distances from the Persian Gulf. Asia, which absorbs over 80 percent of crude oil transiting Hormuz in normal conditions, is already under acute stress. Shipments loaded before the closure have now been consumed, and inventories across the region are shrinking rapidly. India was the first major economy to feel the squeeze, followed by Northeast Asian importers such as China, Japan, and South Korea. JPMorgan projects that Southeast Asian oil demand will contract by roughly 300,000 barrels per day in April. If strategic reserve releases remain limited to individual country efforts, those losses could exceed 2 million barrels per day in May and approach 3 million barrels per day by June.

The Philippines became the first country in the world to formally declare a national energy emergency. President Ferdinand Marcos Jr. signed Executive Order 110 on March 24, citing an imminent danger to the country's energy supply. The Philippines imports 98 percent of its oil from the Middle East and had approximately 45 days of fuel reserves remaining as of March 20, down from 55 to 57 days when the war started. The government released 20 billion pesos from the Malampaya gas fund and authorized fuel imports from alternative suppliers including Russia. State-owned Petron Corporation ordered 700,000 barrels of Russian crude under a temporary US sanctions waiver.

Across the wider Asia-Pacific region, governments are implementing emergency conservation measures. South Korea has urged citizens to take shorter showers and charge electronic devices during daylight hours to reduce electricity consumption. On March 27, the country imposed a full ban on naphtha exports for five months, requiring refiners to redirect all volumes to the domestic market in order to protect petrochemical manufacturing. Japan announced its largest-ever release of strategic oil reserves and reassured citizens that consumer goods hoarding was unnecessary. China has restricted overseas shipments of fuel and other materials to protect domestic inventory. Roughly 5 percent of global ethylene production capacity in Japan, South Korea, and China has already been shut down due to naphtha and LPG shortages, directly impacting plastics manufacturing.

Africa is next in the shockwave sequence. JPMorgan analysts expect the impact to become visible in early April, particularly in nations with low inland inventories and heavy dependence on imported petroleum products. Oil demand losses across the continent could reach 250,000 barrels per day in April if stockpiles run thin.

Europe is projected to feel the pressure by mid-April, though the nature of the shock differs from Asia. European exposure is driven more by rising costs and intensified competition with Asian buyers for non-Gulf crude, rather than direct physical shortages. Having already pivoted away from Russian pipeline gas and crude since 2022, Europe now finds that its alternative Gulf suppliers are constrained or being outbid. The continent has fewer alternative supply routes and less strategic petroleum reserve depth than its Asian competitors. European natural gas prices have jumped to around 55 to 58 euros per megawatt-hour, and airlines operating in Europe face severe pressure from surging jet fuel costs.

North America is the last major region in the shockwave timeline, with most Gulf oil shipments expected to stop arriving around April 15. However, JPMorgan analysts assess that the United States is unlikely to face direct physical shortages in the near term thanks to its massive domestic crude production capacity. The impact on the US economy will manifest primarily through rising fuel prices and dislocations in the refined products market. US benchmark WTI crude has surged over 40 percent in March but remains roughly 10 dollars below the global Brent benchmark, which closed at 108.01 dollars per barrel on March 27.

Gulf producers are attempting to reroute supply through alternative infrastructure. Saudi Arabia has ramped up exports through its East-West pipeline to the Red Sea port of Yanbu, increasing flows from 0.8 million barrels per day to 3.3 million barrels per day, with potential to reach 4.7 million barrels per day by April. The UAE has raised throughput on its Fujairah bypass pipeline from 1.1 to 1.6 million barrels per day. Despite these efforts, the workarounds replace only a fraction of the lost capacity, as the existing infrastructure was never designed to handle a simultaneous outage of this scale.

The International Energy Agency announced a coordinated release of 400 million barrels of oil from strategic reserves across its 32 member nations, the largest such release in the organization's history. IEA chief Fatih Birol described the current disruption as the biggest threat to energy security in history, worse than the two oil shocks of the 1970s and the Russia-Ukraine war combined. The US administration is contributing nearly half of the planned IEA release from its Strategic Petroleum Reserve.

On March 26, President Donald Trump announced a 10-day extension of his pause on strikes against Iranian energy infrastructure, pushing the deadline to April 6 at 20:00 Eastern Time. The move was framed as a response to an Iranian government request and as a window for ongoing negotiations. Trump also claimed that Iran had allowed 10 oil tankers to pass through the Strait of Hormuz as a goodwill gesture. Iran, however, denied that formal negotiations were taking place and stated it was awaiting a US response to its own counter-proposals.

Macquarie Group strategists, led by Vikas Dwivedi, assigned a 40 percent probability to a scenario in which the conflict extends through June. Under that scenario, Brent crude could surge above 200 dollars per barrel and US retail gasoline prices could reach approximately 7 dollars per gallon, levels that would destroy a historically large amount of global oil demand. Macquarie raised its year-end Brent forecast to 89 dollars per barrel but noted that the Brent futures curve, stretching from around 110 dollars down to the 80-dollar range, suggests the market is still pricing in a relatively short conflict resolution.

Energy research firm Wood Mackenzie warned that an average Brent price of 125 dollars per barrel sustained throughout 2026 would be sufficient to trigger a global recession. The conflict has already produced cascading effects across multiple sectors. Aviation is under severe pressure as jet fuel costs account for more than 20 percent of airline operating expenses. Diesel shortages are constraining agriculture, construction, and heavy transport, sectors with no rapid substitution options. Several Southeast Asian countries have implemented emergency measures including work-from-home mandates, reduced speed limits, and license plate-based driving restrictions to curb fuel consumption.

The crisis has also reshaped geopolitical energy dynamics. Russia's land-based export corridors have gained relative attractiveness as maritime risk premiums surge, strengthening Moscow's bargaining position in Asian energy markets. US LNG is emerging as the only supply source that is both scalable and politically reliable for both Asia and Europe, reinforcing American dominance in global energy trade.

💡 Alternative Solution

Saudi Arabia East-West pipeline rerouting via Yanbu (capacity ramped from 0.8 to 3.3 million barrels per day), UAE Fujairah bypass pipeline (raised to 1.6 million barrels per day), IEA coordinated strategic reserve release of 400 million barrels across 32 member nations, US Strategic Petroleum Reserve release, alternative crude sourcing from Russia and non-Gulf producers, national energy conservation mandates across Asia, Omani deep-water ports of Duqm and Salalah as bypass options outside the strait